Bubble Talk

Deen Khan

This is the first of a two-essay series. This essay asks whether AI we’re in a bubble. The next considers what to build in light of that answer.

The Respectable Heresy

The other night on primetime Bloomberg a guest called for the two largest AI labs to be barred from going public. They are dangerous, money-losing companies, he said, and their listings will do nothing but cash out their backers and leave ordinary investors to take the fall. What was surprising wasn’t the argument, but where it was being made. For much of the past few years that kind of contempt lived at the edges: whispered on cable (shouted on X) and waved off by almost everyone “in the know”. Now it led the hour.

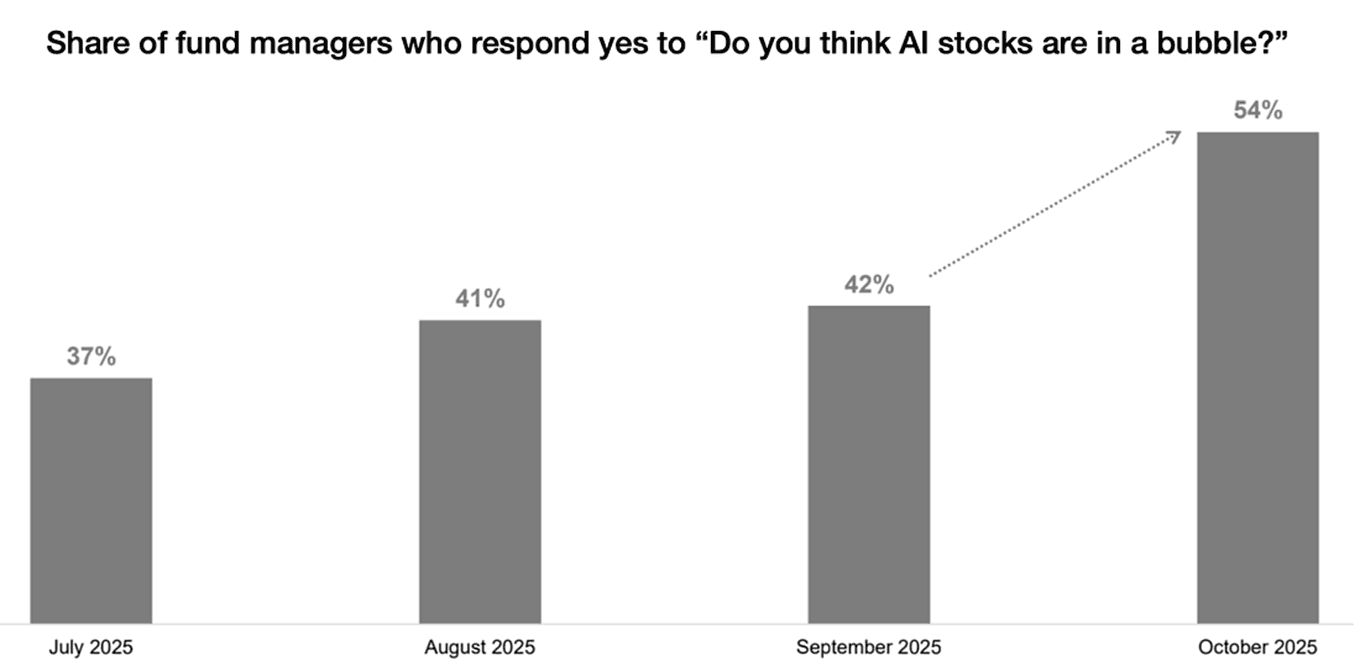

Somewhere in the second half of last year, it stopped being impolite to say “bubble”. A year ago the word belonged to the sceptics - the people who, we were told, simply didn't get it. Then it began to seep inward. In August, Sam Altman accepted that investors as a whole were ‘overexcited’. By October, Jeff Bezos was calling it an ‘industrial bubble’, and Goldman's David Solomon likened the moment to the late nineties (worrying about bubbles is nothing new - Greenspan warned of "irrational exuberance" back in 1996, years before the bubble burst.). Bank of America had taken to asking fund managers outright whether AI stocks were in a bubble:

So, the mood has turned. But a mood is not an argument, and the stakes are real: a dot-com level crash would erase twentyish trillion dollars of American household wealth, the better part of a year's output. It’s worth getting right.

The Clock and the Conflict

Maybe nothing changed but the calendar. Give it enough time and a loud enough chorus, and it will be in vogue to call anything a bubble. But that can't be the reason, because the verdict won’t sit still. In October, most fund managers called it a bubble. By February, fewer than half did. By May they’d mostly stopped worrying about it and cycled back to older fears like inflation and war.

Maybe it’s just self-interest. The people who own these stocks insisting all is well, the people betting against them crying bubble. But the views don’t line up with the bets. Builders with the most to lose said it first; the oldest venture firms are split down the middle, one warns the industry is spending six hundred billion dollars a year more than it can hope to earn back, another calls this the start of a decades-long boom. If money decided the matter, the people with the most to gain would all agree – and they don’t. So, that leaves the real question: are we in a bubble?

The Numbers That Argue With Themselves

The truth is that the people who’ve looked hardest can't agree, because the same numbers point both ways.

Start with the case for alarm. AI-related companies have gone from about a quarter of the S&P 500 to nearly half in three years, and most of America's market gains now trace to a handful of them. So does most of its growth: in the first half of 2025, spending on data centres and computing gear drove ninety-two per cent of GDP growth.

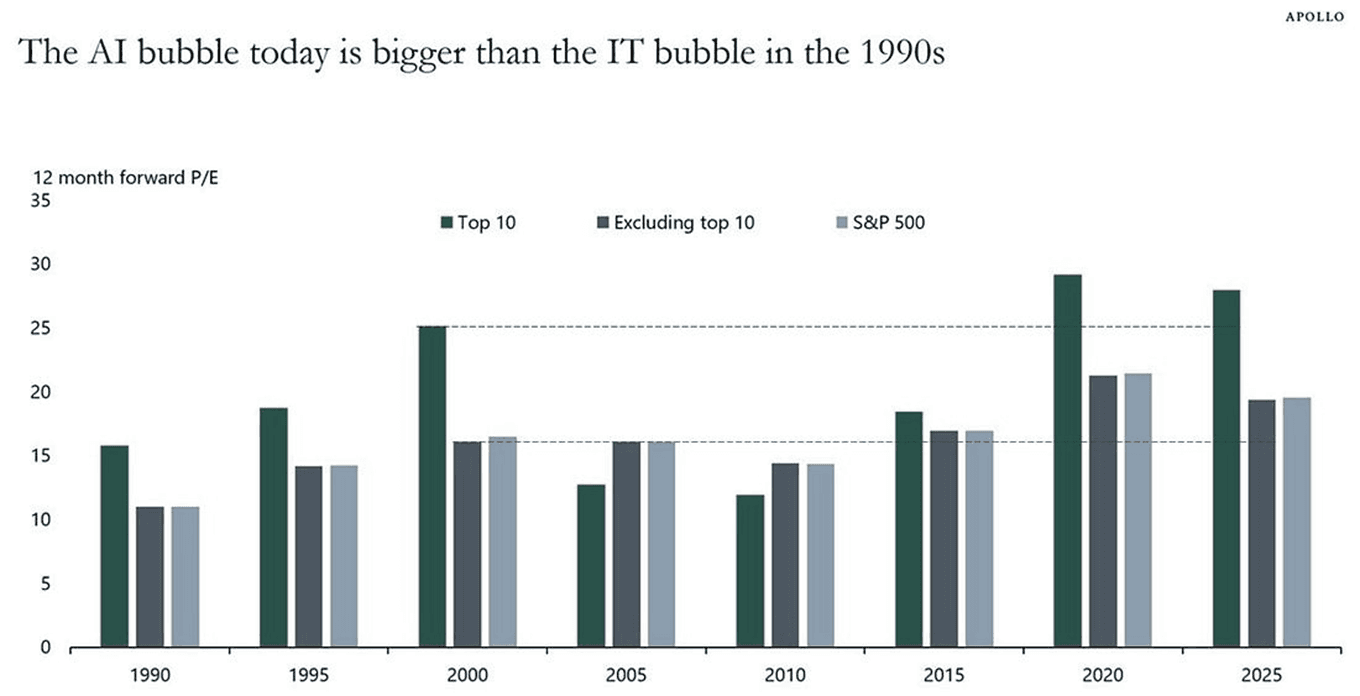

The ten largest are more richly priced than the ten largest were at the peak in 1999, and because so much money simply tracks the index, almost everyone owns the same few companies whether they meant to or not.

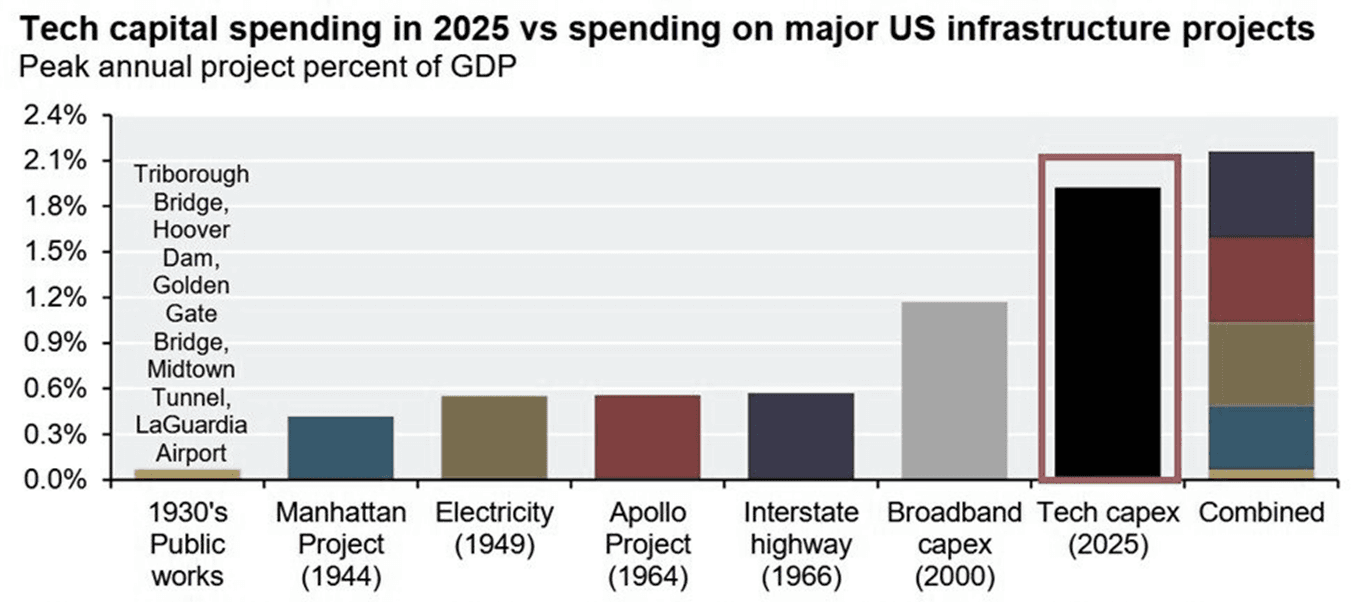

The spending behind it is massive. As a share of the US economy, AI spending this year is bigger than the Manhattan Project, Hoover Dam, Apollo programme, interstate highways and broadband boom, combined. It’s also no longer just a stock-market bet. Hyperscalers now borrow more than anyone else in the investment-grade bond market (more, even, than the banks), which means that if the bet sours, the pain won't stop at the stock market.

Some of that money goes in circles. Nvidia invests in OpenAI; OpenAI spends it on Nvidia chips, which run in data centres Nvidia part-owns. Everyone counts it as revenue. Some of what looks like demand is the same dollar going round the track, and when the same few companies are both the buyers and the sellers, a problem at any one of them is a problem for all of them. It's an old trick: in the dot-com years, telecom-equipment makers lent their customers the money to buy their gear, booking the same dollar as a sale on one side and a loan on the other.

Some of the valuations are hard to read as anything but mania. SpaceX went public claiming a market worth twenty-eight trillion dollars - twenty-six of it in AI - on the strength of an AI business that made about three billion last year. Even Google, which generates more cash than almost any company alive, just sold eighty-five billion dollars of equity to keep up. And the mania attaches to anything: Allbirds recently announced it was abandoning shoes to rent out AI computing power, and its stock rose nearly six hundred per cent in a day - the old 1999 trick of bolting "dot-com" onto your name, in a new suit.

And yet the same figures, read by people every bit as informed, are reassuring. The Nasdaq-100 trades around twenty-eight times forward earnings, not the eighty-nine times of 1999. The indexes are concentrated for a reason: these are the most profitable businesses in the world, earning a much larger share of all profits than the dot-com leaders.

Where dot-com telcos borrowed heavily and dragged the industry down when they fell, today's giants have mostly funded AI out of money they already make (that’s starting to change, but they remain far less stretched than the telecoms were).

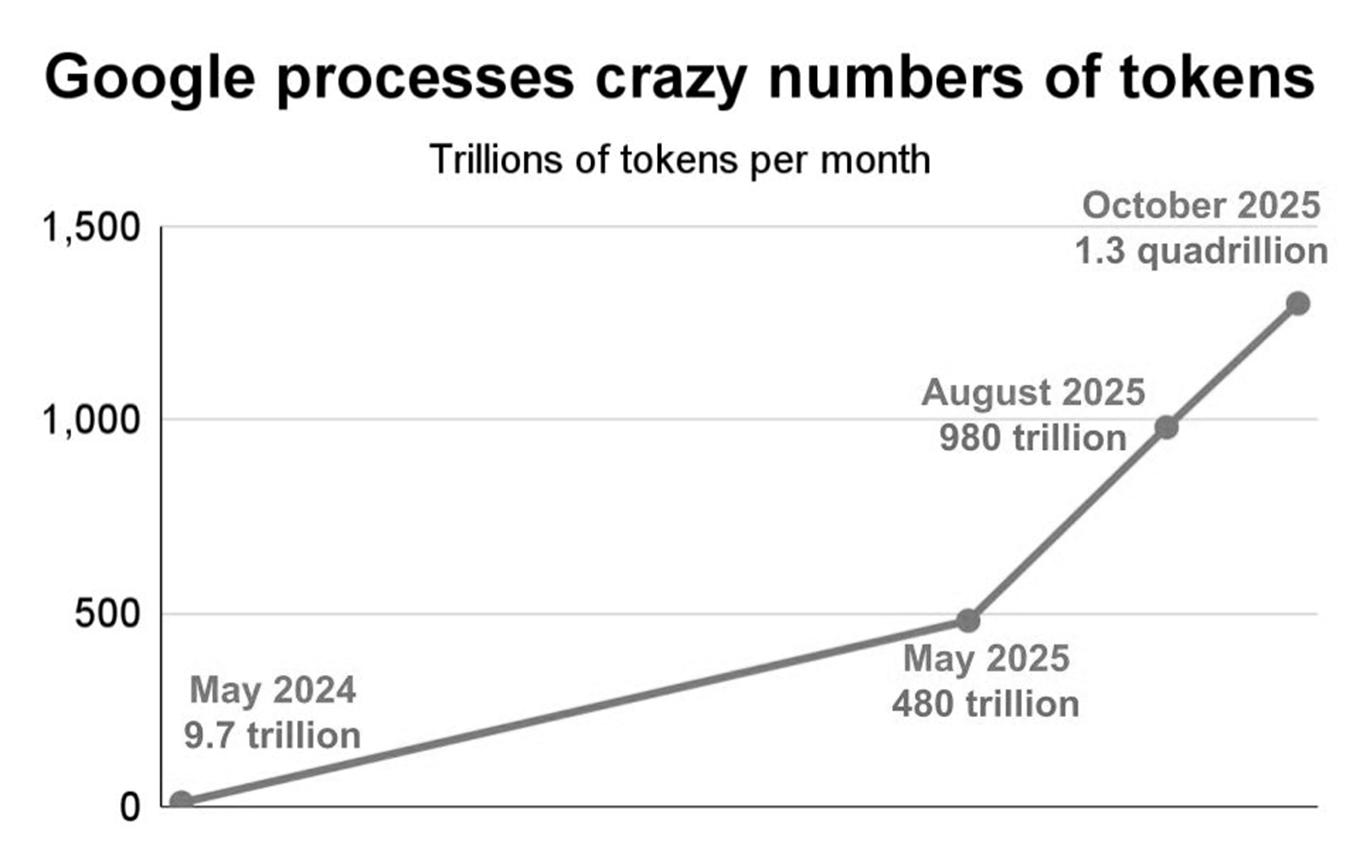

What the optimists really lean on, though, is demand. We've never seen valuations climb like this, but we've never seen demand climb like this either. Over the last year and a half, the tokens these systems handle each month have gone from about ten trillion to more than a thousand trillion - a Lord of the Rings for every person on Earth, every month. And that is only today. Goldman expects the world's token use to grow twenty-four-fold by 2030, as always-on AI agents replace asking one question at a time. The revenue is real, too, not promised: between them, OpenAI and Anthropic went from almost nothing to fiftyish billion in annual revenue in a few years, one product - Claude Code - reaching a billion in six months. Demand keeps outrunning supply, too: data centres are about ninety-nine per cent full, and more than nine in ten still being built are leased before they open. Far from overbuilding, the industry can't build fast enough - the chipmakers are years behind their orders.

Until the Data Confesses

Torture the numbers long enough and they’ll confess to whatever you came for. The bears and the bulls reach opposite conclusions from the same figures, because the figures can support both. So, we may be asking the wrong question. A better one would be: not whether this is a bubble, but whether it would matter if it were.

The Useful Kind of Catastrophe

Suppose it's a bubble. The funny thing about bubbles is that they are often how the future gets built. Carlota Perez has shown how this usually goes. A wave of speculative money builds far more infrastructure than anyone yet needs; the bubble bursts and the speculators are wiped out; and the infrastructure stays behind, cheap, for whoever comes next. The dot-com bubble left very few dot-coms, but it did leave fibre - tens of millions of miles of it, laid by telcos that died in the process. WorldCom alone laid a hundred thousand miles before going bankrupt under forty billion dollars of debt; its fibre was sold for pennies, and by 2010 it carried most of America's internet traffic, including streaming that didn't exist when it went into the ground. The bandwidth was nearly free because the companies that laid it had gone bankrupt.

The obvious objection is that plenty of bubbles leave nothing behind. Tulips left nothing. The housing bubble left foreclosures. The difference is what the money is betting on. Some bubbles are pure mania, a game of passing assets to a greater fool. These leave only losses. Others are bets that the future will be different - railways, electricity, fibre - and these lay the rails of that future even as they ruin some of the people laying them. They work by getting many people to build toward the same future at once: when one set of investors commits to a vision, it makes the next piece safer for everyone else to build. It is telling that Bezos called this an “industrial bubble” - the productive kind, that leaves something behind.

These bubbles leave behind more than cable and steel; they also leave knowledge. The dot-com years wired the country and put a generation online, teaching it to build for the web - which made the software industry that followed possible. Advances that would have come one at a time over decades came all at once, because everyone was working on the same thing at the same time. The same is happening now: most of the global technology industry is building on AI at once, and the gains compound - better models make more applications worth building, which earns the revenue that pays for more infrastructure, which trains better models.

So what will this bubble leave behind? Probably not the chips. The fibre from the dot-com bust sat cheap in the ground for decades; a data centre is a different animal - its processors wear out in a few years, and it burns money just to keep running, on power and cooling and replacements. No one will inherit what's being spent on the chips. But two things will last. The first is power. The thing that most limits AI now is electricity, and the rush to supply it is building an enormous amount of new power - much of it solar and nuclear, which costs almost nothing to run once it's built. When the companies that overbuilt go bust, the cost of building all that power dies with them. The power stays, cheap and clean, for decades. If the boom did nothing else, that would be enough. The second is intelligence itself. Some of this money is being spent to train powerful models and then give them away, the weights published for anyone to download and build on. An open model is a strange asset: it costs a fortune to make and almost nothing to copy, and unlike a chip it never wears out. Once it's released, the fortune spent training it becomes a gift to everyone who comes after. Each open model is soon overtaken, but the floor it sets stays put. So whatever gets built next starts with cheap power, trained people - and frontier-grade intelligence that's free to build on.

None of which makes bubbles harmless. Not all of them are productive; the productive ones aren't productive right away; and none of it happens without a great deal of waste and ruin along the way. And being right is no protection. You could have seen the whole future of the internet and still been wiped out in the crash: Amazon fell about ninety-five per cent, Cisco and Oracle nearly as far, and anyone who had borrowed to hold them didn't last long enough to be proved right.

Voting and Weighing

So where does this leave anyone trying to decide whether to build, or to back the people who do? Benjamin Graham had a line for it: in the short run the market is a voting machine, in the long run a weighing machine. A bubble is the voting - what the crowd thinks a price is worth today, which matters enormously if you have to sell tomorrow. The companies that last are settled by the weighing, and that takes years. Amazon, Google, Salesforce and Netflix were all founded around the dot-com bubble. The crash hammered every one of them. And every one, in the end, turned out to be worth a fortune. Far from stopping them, the bubble is part of what made them - the cheap infrastructure, the trained engineers, the rush of people all building at once.

Which gives an answer, and it is the same answer down either path. If this is not a bubble, the fundamentals are sound and the course is obvious: build. If it is a bubble, it is the useful kind - laying down the power, the open-source models and the people that the next decade will inherit - and the course is exactly the same: build. The question that’s consumed everyone for a year turns out not to be the one that matters.

It helps to remember how badly the smart money has read these moments before. Three weeks after Lehman fell, Sequoia gathered its founders, showed them a slide of a gravestone reading "RIP, Good Times," and told them to brace for a generational contraction and a long VC winter. The recovery took a while, but the decade that followed was one of the best in the history of startups. A few months after that gravestone, Airbnb was funded; a few months later, a company called UberCab got going. Of the eight thousand internet companies funded during the bubble, almost none survived to 2010 - and the few that did, together with the wave built on the wreckage they left behind, became the most valuable companies on earth.

So the question worth asking was never whether this is a bubble. It's what the bubble is building - and what to do about it. The cheap power, the open models, the trained engineers: what they get used for is almost never what they were funded for. That is where the real work begins, and where this series goes next - how to build on it, from first principles.